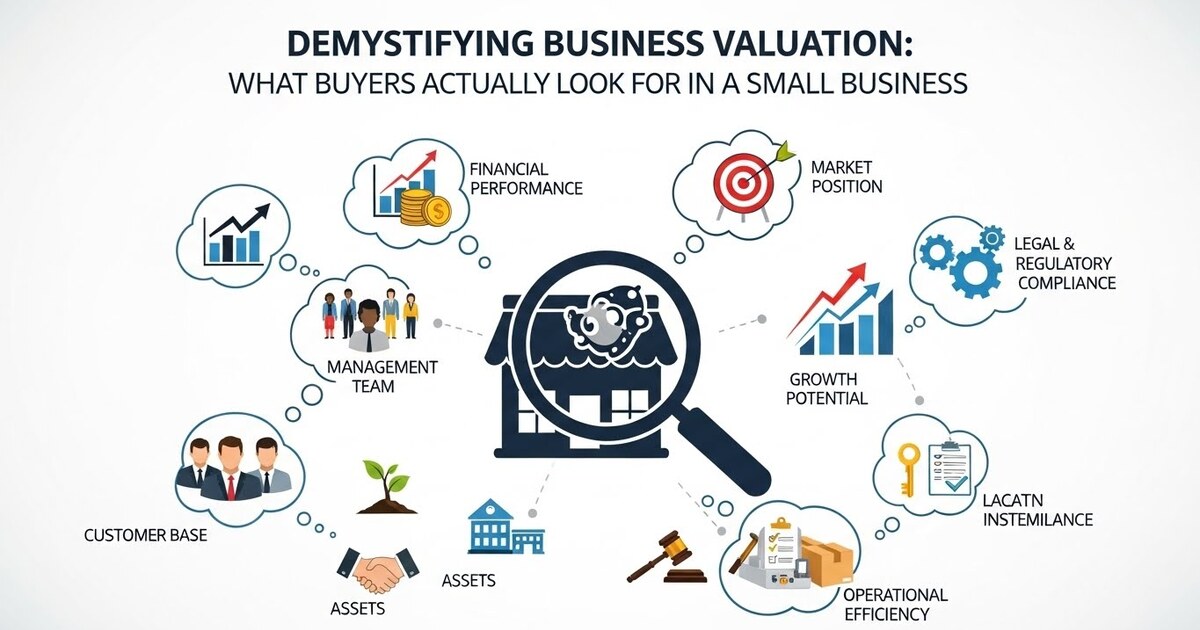

Demystifying Business Valuation: What Buyers Actually Look For in a Small Business.

There is a profound disconnect in the world of small business.

The business owner looks at their company and sees the “Sweat Equity.” They see the missed birthday parties, the late nights, the risk taken in 2015 when the bank account hit zero, and the loyal culture they built from scratch. To them, the business is priceless or at least worth a fortune.

The buyer looks at the same company and sees none of that. They see a spreadsheet. They see risk. They see a machine that either generates cash or consumes it.

This disconnect is why deal fatigue sets in. It is why founders walk away from negotiation tables insulted, and why buyers walk away confused.

Valuation is not an art, and it is not a reflection of your personal worth. It is a cold, hard financial calculation based on Risk and Return. If you want to maximize your exit, you must stop thinking like a “Parent” (who loves the baby unconditionally) and start thinking like an “Investor” (who wants a return on capital).

This guide demystifies the black box of valuation. We will strip away the jargon and explain exactly what buyers look for, how they calculate the check size, and how you can influence the math in your favor.

I. The Fundamental Equation: The Math Behind the Check

Before we discuss “intangibles,” we must understand the base formula. Almost every small business valuation boils down to this equation:

$$\text{Valuation} = \text{Profit Metric} \times \text{The Multiple}$$

It looks simple, but both variables are battlegrounds.

1. The Profit Metric: SDE vs. EBITDA

What counts as “Profit”? It depends on the size of your business.

A. Seller Discretionary Earnings (SDE)

- Used for: Businesses with under $5M in revenue (Main Street businesses).

- The Logic: In small businesses, the owner often pays themselves a salary, runs their car through the business, and pays for personal health insurance. SDE adds all these benefits back to show the true earning power of the business for a new owner-operator.

- Formula: $$\text{SDE} = \text{Net Profit} + \text{Owner’s Salary} + \text{Personal Expenses} + \text{One-Time Expenses}$$

B. EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

- Used for: Businesses with over $5M in revenue (Lower Middle Market).

- The Logic: At this size, the buyer (often a Private Equity firm) will likely hire a CEO to run it. Therefore, the owner’s salary is a real expense, not an add-back. EBITDA measures the pure operational cash flow.

2. The Multiple

This is the multiplier applied to your profit.

- If your SDE is $500,000 and the multiple is 3x, your business is worth $1.5 Million.

- If your SDE is $500,000 and the multiple is 5x, your business is worth $2.5 Million.

The million-dollar question: What determines if you get a 2x or a 6x?

The answer: Risk.

II. The 4 Drivers of the Multiple (What Buyers Scrutinize)

Buyers use the Multiple as a risk-adjustment tool. A high multiple means “Low Risk / High Growth.” A low multiple means “High Risk / Stagnation.”

Here are the four lenses buyers use to determine your multiple.

Driver 1: Financial Integrity (The “Trust” Factor)

If a buyer cannot trust your numbers, they will not buy your business. Period.

- The Shoebox Problem: If you run your business out of a shoebox of receipts and commingle personal and business funds, your valuation tanks.

- Audited/Reviewed Financials: A buyer loves “Accrual-based accounting” (GAAP). It shows they are buying a professional entity.

- The Trend Line: $500k profit on a downward trend is worth significantly less than $500k profit on an upward trend.

- Scenario A: Year 1 ($200k), Year 2 ($350k), Year 3 ($500k). Verdict: High Multiple.

- Scenario B: Year 1 ($700k), Year 2 ($600k), Year 3 ($500k). Verdict: Low Multiple (Falling Knife).

Driver 2: Transferability (The “Bus Test”)

We touched on this in previous articles, but in valuation, this is quantified.

- Owner Dependency: If you are the lead salesperson and the lead technician, the buyer has to hire two people to replace you. That cost comes directly out of the EBITDA, lowering the valuation.

- Key Employee Risk: If your Head of Sales holds all the client relationships and has no non-compete agreement, that is a massive risk. If they leave post-sale, the revenue evaporates.

Driver 3: The “Moat” (Defensibility)

What stops a competitor from stealing your lunch tomorrow?

- Weak Moat: “We offer great service.” (Everyone says this).

- Strong Moat:

- Exclusive Contracts: “We have the exclusive distribution rights for Brand X in Texas.”

- Intellectual Property: “We own the patent for this widget.”

- High Switching Costs: “Our software is integrated into their daily workflow; it would take them 6 months to switch.”

- The Valuation Impact: A business with long-term contracts (Recurring Revenue) commands the highest multiples in the market.

Driver 4: Customer Concentration (The “One-Legged Stool”)

This is the most common deal killer.

- The Metric: If any single customer accounts for more than 15% to 20% of your revenue.

- The Buyer’s View: “If I buy this business for $5M, and Customer A (who is 40% of revenue) leaves next month, I just lost $2M of value.”

- The Penalty: Buyers will structure the deal as an “Earn-out.” They will pay you part of the money now, but withhold the rest for 2-3 years to ensure that big customer stays.

III. The Tale of Two Buyers: Strategic vs. Financial

Not all money is green in the same way. The type of buyer determines the valuation ceiling.

1. The Financial Buyer (The “Spreadsheet” Buyer)

- Who they are: Individual investors, Search Funds, or Private Equity Groups (PEGs).

- What they want: Cash flow. They want to buy your business, pay off the debt, and make a return on their investment.

- Valuation Cap: They are bound by math. They cannot pay more than the business’s cash flow can support in debt service. They typically pay Market Value (e.g., 3x – 5x SDE).

2. The Strategic Buyer (The “Synergy” Buyer)

- Who they are: Competitors, Suppliers, or Large Corporations in your industry.

- What they want: Your customer list, your technology, or your location.

- Valuation Cap: They can pay Above Market Value (e.g., 6x – 10x+ EBITDA).

- Why? Because of Synergy.

- Example: If a Strategic Buyer has a sales team of 500 people and buys your product, they can plug your product into their sales machine and triple your sales overnight. Your $1M profit is worth $3M to them. They pay you for that potential.

Key Takeaway: The “Life Changing Money” exits almost always come from Strategic Buyers. To attract them, you must build something unique (Product/IP) rather than just a profitable service shop.

IV. The Dark Art of “Add-Backs”

In small business M&A, the negotiation often revolves around the “Add-Back Schedule.” This is your chance to prove that your profit is higher than your tax return shows.

Legitimate Add-Backs (Buyers Accept):

- Owner’s Compensation: If you pay yourself $200k but a replacement manager costs $100k, you can add back the difference.

- Personal Auto Leases: The company G-Wagon.

- Discretionary Travel: The “Board Meeting” in Cabo San Lucas.

- One-Time Legal Fees: Costs for a lawsuit that is now settled and won’t recur.

Aggressive Add-Backs (Buyers Reject & Get Annoyed):

- “Marketing Experiment”: “We spent $50k on Facebook ads that didn’t work, so add that back.” (No, that’s a failed business expense).

- Under-market Rent: If you own the building and don’t charge the business rent, the buyer will subtract “Fair Market Rent” from your profit, lowering your valuation.

V. The Red Flags: Why Buyers Walk Away

Even if the math looks good, “Due Diligence” is where skeletons come out of the closet.

- Undocumented Cash: “We make $100k more in cash that we don’t declare to the IRS.”

- Buyer Response: “I cannot pay you for earnings you proved didn’t exist to the government. That is illegal and unverified.”

- Messy CAP Table: You promised 5% equity to an old developer 4 years ago via email but never formalized it. That developer can sue the buyer later. Deal killer.

- Pending Litigation: Any active lawsuit is usually a hard stop until resolved.

- Declining Gross Margins: If revenue is going up but your profit margin is going down, it means you are buying sales (lowering prices to grow). This signals a weak business model.

VI. Conclusion: Valuation is a Management Tool

You should not wait until you want to sell to get a valuation.

A business valuation is the ultimate “Health Check.” It tells you exactly how the market judges your performance.

- If your multiple is low (2x), it means the market thinks you are risky.

- If your multiple is high (5x), it means the market thinks you are resilient.

Knowing this number today changes how you operate tomorrow. Instead of just focusing on “More Sales,” you start focusing on “Better Sales” (Recurring). Instead of hoarding tasks, you start delegating to increase Transferability.

The goal is to build a business that is so valuable, you have the option to sell it for a fortune—or the pleasure of keeping it because it runs like a Swiss watch.