Profit and Loss Statement Made Easy: Navigating Your Business Finances

As a seasoned entrepreneur, I understand that navigating the financial landscape of a business can be challenging. One crucial tool that has been instrumental in my journey is the Profit and Loss (P&L) statement. In this article, I’ll guide you through the ins and outs of P&L statements and why they are indispensable for any business.

What is a Profit and Loss Statement?

A Profit and Loss Statement, often referred to as an income statement, is a financial report that provides a snapshot of a company’s revenues, costs, and expenses over a specific period. It essentially tells you whether your business is making a profit or incurring a loss.

Components of a Profit and Loss Statement

- Revenue (Sales): This is the total income generated from the sale of goods or services.

- Cost of Goods Sold (COGS): These are the direct costs associated with producing the goods or delivering the services.

- Gross Profit: Calculated by subtracting COGS from Revenue, this represents the profit before accounting for operating expenses.

- Operating Expenses: These include rent, utilities, salaries, marketing expenses, and other costs associated with running the business.

- Operating Income: This is the profit after accounting for operating expenses.

- Other Income and Expenses: This section includes non-operating income and expenses like interest, taxes, and one-time gains or losses.

- Net Income: Also known as the bottom line, this is the final profit or loss figure.

The Significance of Profit and Loss Statements for Businesses

Financial Health Check

A P&L statement provides a clear view of your business’s financial health. It allows you to see if your revenue is covering your expenses and if you’re operating at a profit.

Performance Evaluation

Analyzing trends in your P&L statement over different periods helps in evaluating the performance of your business. Are your profits increasing? Are your expenses well-managed? These are crucial questions that a P&L statement can answer.

Decision-Making Tool

Whether you’re considering expansion, hiring new staff, or introducing a new product line, a P&L statement can provide the financial insights needed to make informed decisions.

Investor Confidence

For investors and stakeholders, a well-prepared P&L statement demonstrates transparency and financial stability. It instils confidence and trust in your business.

How to Create a P&L Statement

Creating a Profit and Loss statement involves several steps:

- Gathering Financial Data: Collect all relevant financial information for the period in question.

- Organizing and Categorizing Expenses: Properly categorize expenses to ensure accuracy in your statement.

- Calculating Revenue and Expenses: Use the appropriate formulas to calculate revenue, COGS, and expenses.

- Formatting the Statement: Present the information in a clear, easy-to-understand format.

Interpreting a Profit and Loss Statement

Analyzing Revenue Trends

By comparing revenue figures over different periods, you can identify growth trends and potential areas for improvement.

Understanding Cost Structures

A detailed look at your expenses can reveal areas where you might be overspending or areas where cost-cutting measures can be implemented.

Assessing Gross and Net Profit Margins

Gross and net profit margins indicate the percentage of revenue that translates into profit. Higher margins are generally indicative of a healthier business.

Identifying Areas for Improvement

A thorough analysis of your P&L statement can highlight areas that require attention. It could be reducing certain expenses, optimizing pricing strategies, or exploring new revenue streams.

Common Mistakes to Avoid

To ensure the accuracy of your P&L statement, avoid common pitfalls such as neglecting accrual accounting, misclassifying expenses, ignoring seasonal trends, and failing to update it regularly.

Real-world Examples and Case Studies

Let’s take a look at a couple of examples to illustrate the power of P&L statements in real-world scenarios:

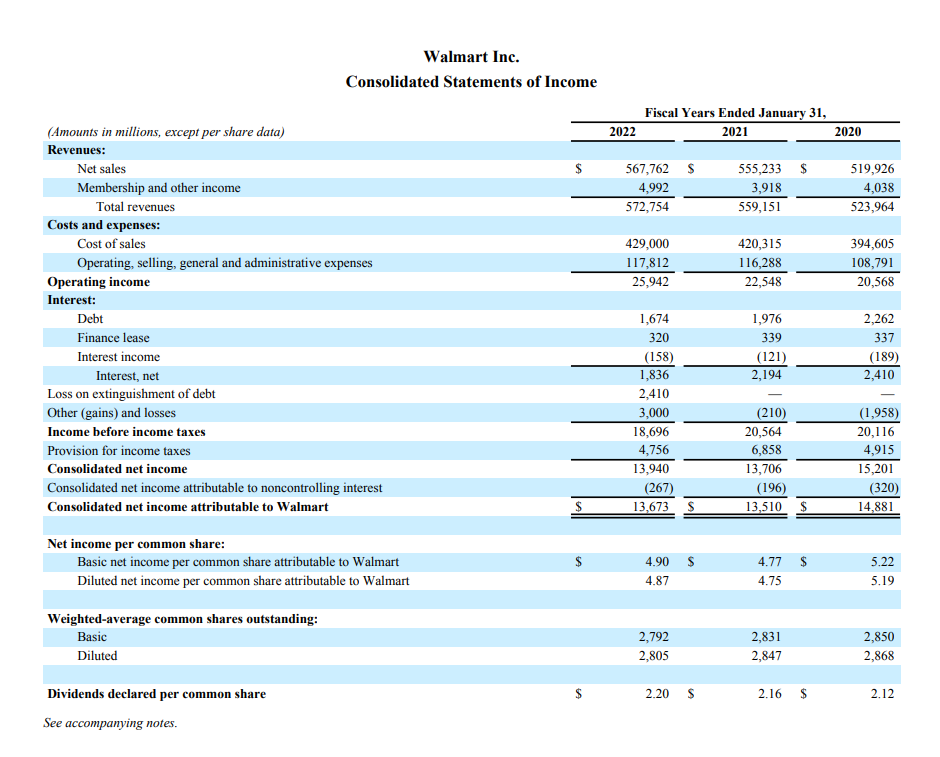

Example 1: Retail Business- Walmart Inc

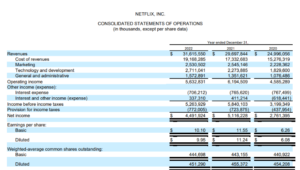

Example 2: Service-Based Business- Netflix Inc

Using Profit and Loss Statements for Strategic Planning

Budgeting and Forecasting

A well-prepared P&L statement forms the basis for budgeting and forecasting, allowing you to set realistic financial goals.

Setting Financial Goals

With a clear understanding of your financial performance, you can set ambitious yet achievable goals for your business.

Long-term Business Planning

P&L statements play a crucial role in charting the course for the long-term success of your business. They provide the data needed to make strategic decisions.

Tools and Software for Creating Profit and Loss Statements

There are various tools and software available, such as spreadsheet programs like Excel or Google Sheets, as well as dedicated accounting software like QuickBooks and Xero. Additionally, you can find templates and resources online to assist you in creating accurate Profit and Loss statements.

Conclusion

In conclusion, a well-prepared Profit and Loss statement is an invaluable tool for any business owner. It provides insights into the financial health of your business, aids in decision-making, and instills confidence in stakeholders. In addition, a well-prepared P&L statement is essential for internal monitoring, external communication, and attracting potential investors. Embrace the power of the Profit and Loss statement, and unlock the insights needed to drive your business towards greater success.